For homeowners who think no news from

the bank means they're on a good rate

The bank gives its lowest rate to the customer who just walked in. Not the

one who's paid on time for years.

I'm Bayley, a mortgage broker. The bank you're with can only ever sell you the rates they have, so of course they say there's nothing better. I check your loan against 26 lenders and tell you straight up whether it's costing you thousandswhether it's costing you thousands. Watch the 2-minute video below, then take the 30-second quiz.

CLICK BELOW TO WATCH FIRST!

Human

NOT BANK

$110m+

LOANS SETTLED

106

5-STAR REVIEWS

26

LENDERS

Let's see what your loyalty's been costing you — takes 30 seconds

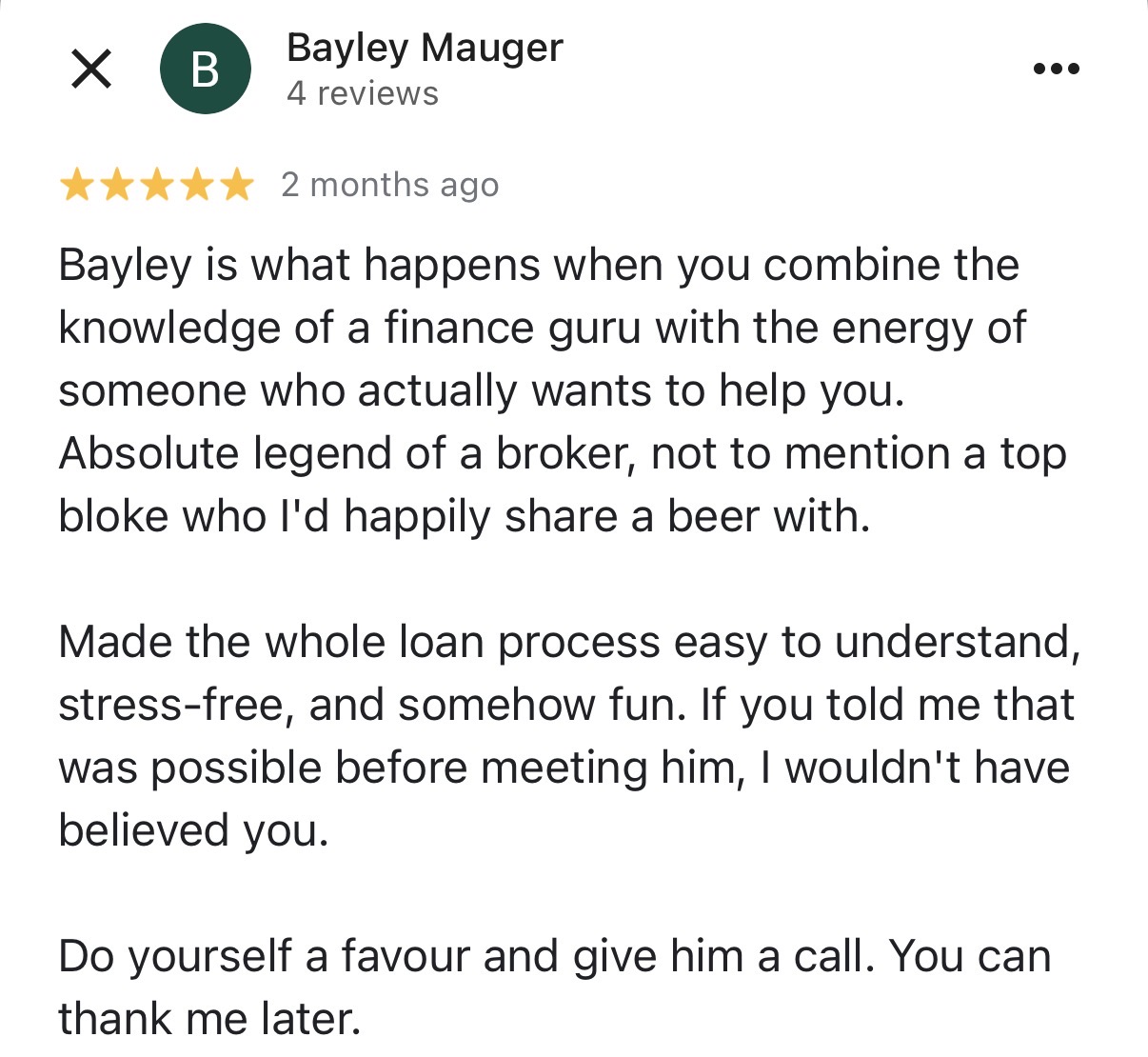

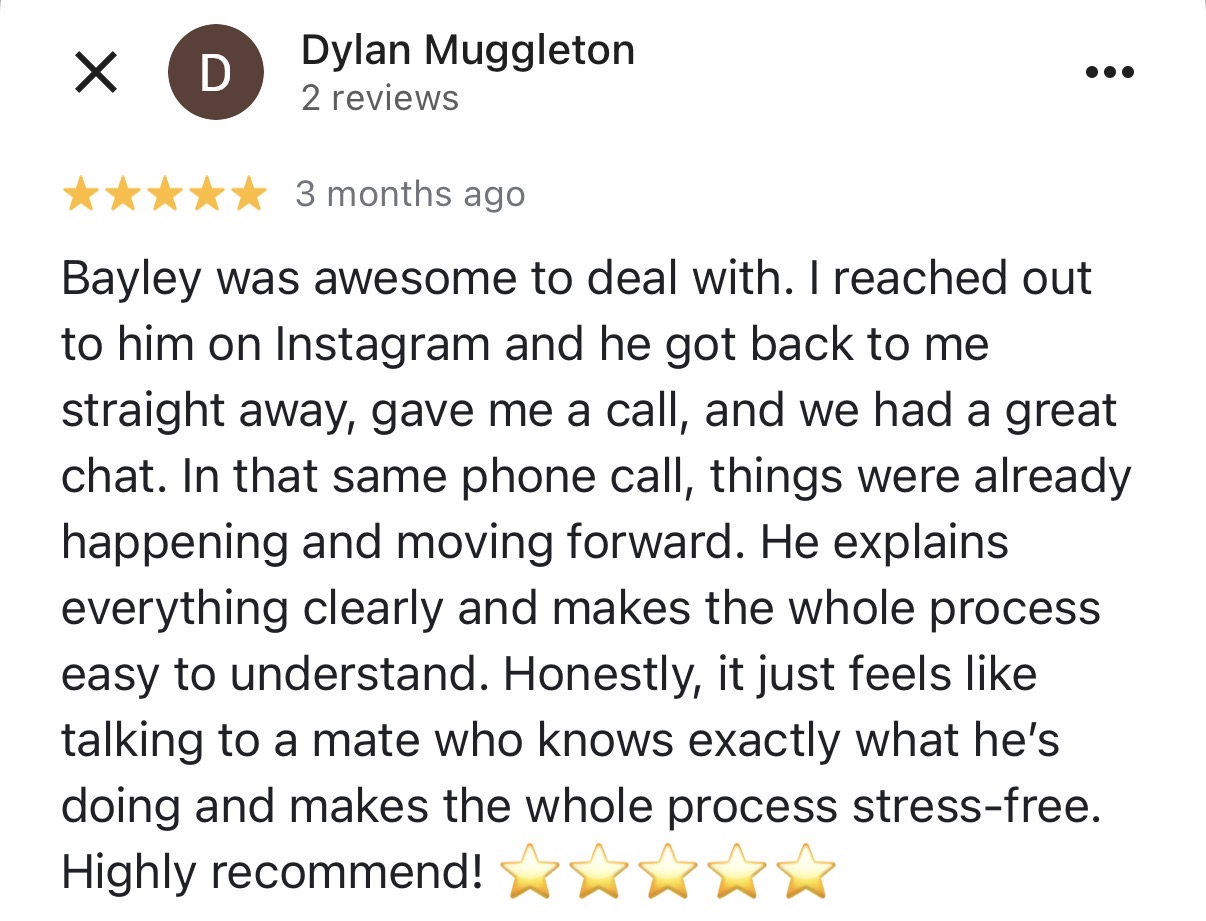

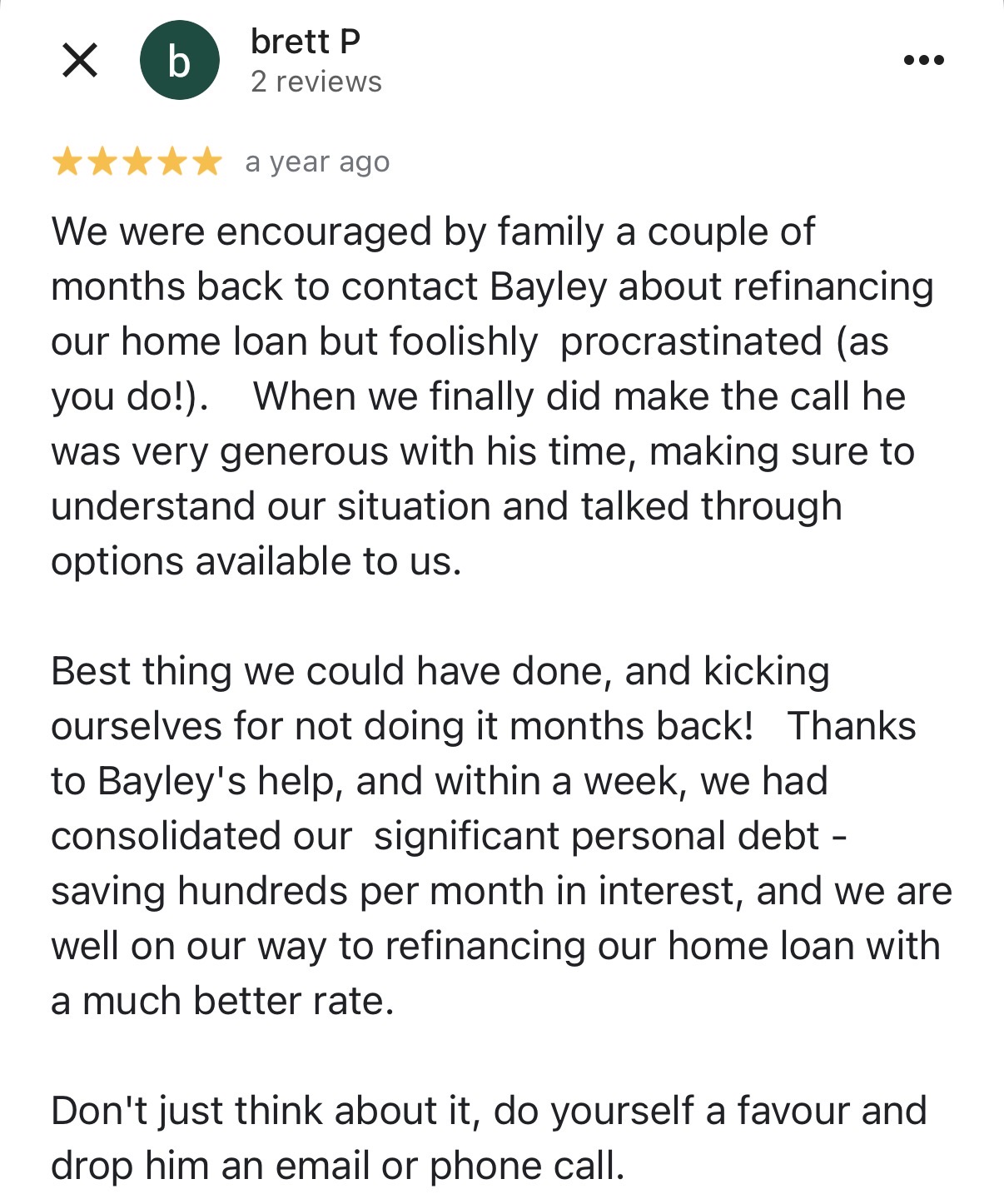

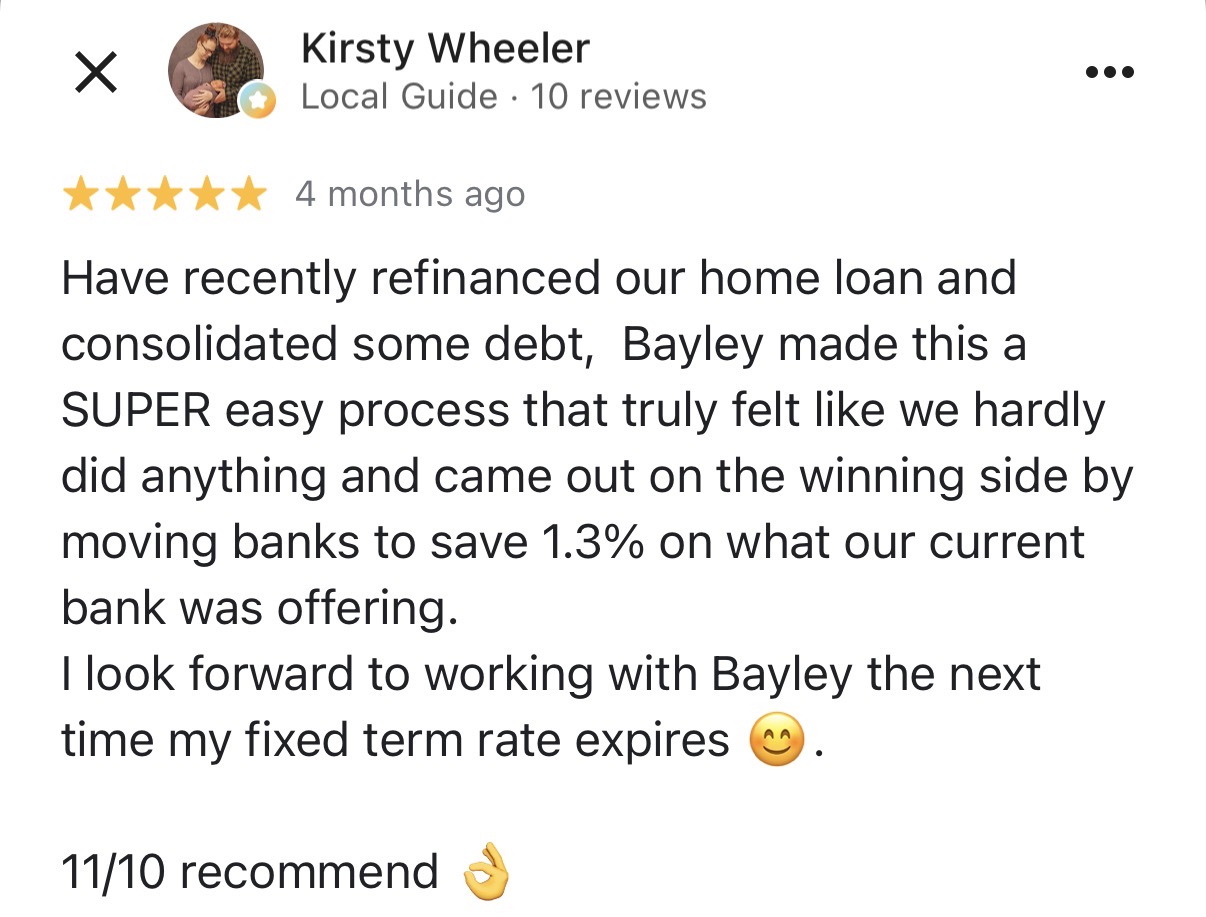

TESTIMONIALS

What others are saying

Real homeowners. Real savings.

For the homeowner who assumed "no news" meant "good rate"

See in plain numbers exactly what staying loyal has cost you

Put the saving into your loan and own your home years sooner

Roll a high-interest debt into your home loan and free up cash every month

Evenings and weekends, on the phone with me, never a call centre

26 lenders checked - not your bank marking its own homework

Switching's about $800, and a lender cash back often wipes even that

STILL NOT SURE?

Frequently Asked Questions

The questions I get asked every week

How much does switching actually cost?

Usually around $800-1000 - mostly government title fees and a discharge fee from your old lender. A lot of the time a lender cashback covers that and ideally we want those fees to be covered within months of your new loan being open to make it financial viable, so you're square within months and ahead every month after. I'll show you the real number before you decide a thing.

Why didn't my own bank tell me about a better rate?

Because the person you ring can only sell you their bank. If there's nothing sharper there, that's all they'll ever say. I'm not owned by anyone - I run your loan across 26 lenders and tell you straight, even if straight is "you're already on a good rate, leave it."

How long before a refinance pays for itself?

Usually months, not years. On a $500k loan, dropping from 6.26% to 5.5% is about $3,750 a year. Against roughly $800 to switch, it pays back fast. I'll put your actual numbers in front of you so it's not a guess.

Can't I just call my bank and ask them to lower it?

You can, and sometimes you should as the retention team has the ability to reduce your rate. But your bank only moves as far as it has to to keep you, and it's marking its own homework. I check their "best offer" against 26 other lenders so you actually know if it's the best. Sometimes the reprice wins and I'll tell you to stay put.

Will my bank try to talk me out of leaving?

Usually, yes - once you ask to discharge, a retention team suddenly finds a rate they could've given you years ago. That's the loyalty tax admitting itself and most of my clients tell them to shove it. By then you'll know exactly what everyone else is offering, so you can take their better number or walk. Either way you win.

Will it hurt my credit score?

I have a look with a soft enquiry initially which does not leave an enquiry on your credit score and leaves your score unaffected. Home loan enquiries are seen as very low risk and with clients I see no noticeable change in credit score from a refinance application

What if I'm on a fixed rate?

Then timing matters more often than not, breaking early can carry a cost, so sometimes the move is to line it all up and switch the day it expires. Tell me when your fixed term ends and I'll tell you straight whether to wait or move now, before your bank quietly rolls you onto their revert rate.

What does it cost me to use you?

Nothing for my help. I'm paid by the lender, the same rate whether you go direct or through me - except I check all of them and you check one. If you're better off where you are, I'll tell you that too.

How much paperwork is involved, really?

Less than you think, and I prep most of it. Typically ID, a couple of payslips or returns, and your current loan statements. I'll send you a short list, you send it back, I handle the rest. Keep it Simple Stupid is my methodology.

What do you need from me to get started?

Just your current rate, lender and roughly what's owing - that's enough for me to tell you on the first call whether it's worth going further. The full document list only comes once we know there's a saving worth chasing.

Should I fix, stay variable, or split?

Depends on what you value - certainty or flexibility - not on what's popular. I'll walk you through what each means for your repayments and we'll pick what fits your life, not the bank's margin.

Is now even a good time to refinance?

The best time is whenever your current rate isn't competitive — that's true in any market. Waiting for the "perfect" moment usually just means more months of loyalty tax. Ten minutes tells you whether it's worth it today.

Can I roll other debts into my home loan?

Often, yes. Folding a high-interest personal loan or card into your mortgage can free up real cash each month. One client rolled a $28k personal loan at nearly 20% into their home loan and breathed again. I'll show you whether it stacks up or just stretches the debt out longer.

Can I pull out equity to renovate or invest?

If you've owned a while, you may be sitting on more than you think. A refinance can unlock that equity for a reno, an investment, or a deposit on the next place. I'll tell you what's actually there and what's worth using.

Will my repayments definitely go down?

Not always the goal. Sometimes we keep the repayment the same and shorten the loan so you own it sooner, or free up cash flow instead. I'll show you both so you choose, rather than assuming lower repayment is automatically the win.

A bank already said no. Is that it?

No. A bank says no to a box you don't fit. I've got 26 lenders, and "no" at one is a "yes" at another all the time. The bank's calculator isn't the final word - that's the whole reason I do this.

How a switch actually works

Step 1 - The 10 minute chat.

You tell me your rate and lender, I tell you straight whether you can do better. No forms first, no homework.

Step 2 - I check all 26 lenders

I run the numbers across the panel and show you the saving, the switch cost, and what's left in your pocket - before you commit to anything.

Step 3 - We get you approved.

I deal with both banks and the paperwork. You get the call that it's done, and the savings roll to you

Meet Bayley

Hey, I'm Bayley

I'm a mortgage broker, and I work differently to a bank. No branch, no call centre, no being passed around - you deal with me from start to finish. I know how frustrating it can be to have to wait on hold to your bank or wait in line at the branch to ask them for a better deal, only to be told no.

That's the reason I do this. I'd rather sit down with someone who's been there isn't a lower rate and do the shopping for them. I'll always tell you straight where you stand and if there is a better deal out there to not. If not, brilliant. If so, then let's stop letting the bank make the most profit off us.

You'll also notice I don't work from an office. I run everything from my van - and no, I won't be parking it in your driveway. It just means I work online and over the phone, from wherever I am, so I can help you whether you're in the city or three hours from the nearest branch. It also means I've got the time to look at your situation properly, instead of running it through a calculator and giving you a yes or no in thirty seconds.

That's the difference: I'll actually look at your situation, not just a number on a screen.

$110m+ in home loans settled

106 five-star reviews, almost all word of mouth

26 lenders, so one bank's "no" is never the end of it

Find out what your loyalty has been costing you

10 minutes on the phone and I'll tell you straight whether you can do better

Same repayment, years off your loan OR the same loan term, hundreds back in your pocket each month. Your call.

Bayley the Broker · 0437 189 939 · [email protected]

Bayley Clarke ABN 93 663 382 974. Credit Representative of Lendi Pty Ltd, Australian Credit Licence 246786.

Your full financial situation will need to be reviewed prior to acceptance of any offer or product. Subject to lender terms, eligibility and criteria.